If you’re exploring a USDA loan for new home construction in Indiana, most of what you’ll find is either government policy language written for program administrators or national mortgage guides with no local context. This post is different. It’s written for buyers in Southwest Indiana who are considering building a new home and want practical, local guidance on whether USDA financing fits their situation.

Key Takeaways

- USDA loans offer 100% financing for eligible buyers, meaning no down payment required.

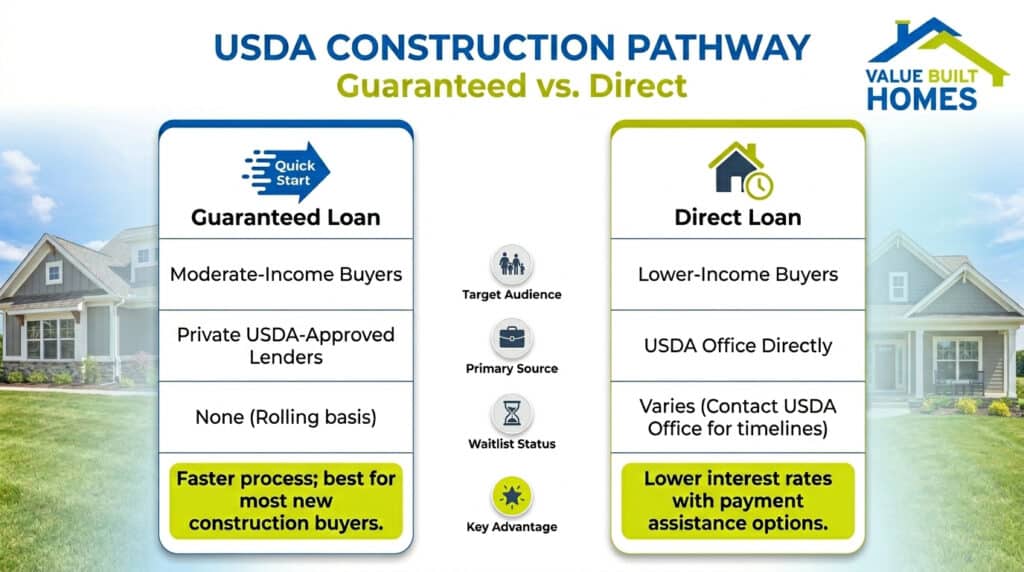

- Two programs exist: the Guaranteed Loan (for moderate-income buyers, no waitlist) and the Direct Loan (for lower-income buyers; processing times vary by location and funding availability; contact the Jasper Area Office for current timelines in Southwest Indiana).

- For most buyers in Southwest Indiana, the USDA Guaranteed Loan is the more accessible and practical path.

- USDA financing can be used for new construction through a single-close construction-to-permanent loan, but only a limited number of lenders nationally offer this option.

- Value Built Homes builds site-built homes with floor plans priced from $128,500 to $238,000, a range that aligns well with what USDA-eligible buyers in this region can finance. Value Built Homes is the builder; buyers work with a USDA-approved lender for financing.

- Rural area eligibility must be verified for your specific address using the USDA’s online property eligibility map.

What Is a USDA Loan?

A USDA loan is a government-backed mortgage offered through the U.S. Department of Agriculture’s Rural Development program. It helps low- to moderate-income buyers purchase homes in eligible rural and suburban areas with 100% financing, no down payment required, and competitive interest rates.

Despite the name, USDA loans aren’t limited to farmland or remote countryside. Many small towns and suburban communities across Indiana qualify. The program is for primary residences only, not investment properties or vacation homes.

USDA Guaranteed vs. Direct: Which Program Applies to You?

Two separate programs fall under the USDA rural housing umbrella. They serve different income tiers and work through different channels. Knowing the difference matters before you start the process.

USDA Single Family Housing Guaranteed Loan Program

The Guaranteed Loan is issued through USDA-approved private lenders, similar to how FHA or VA loans work. USDA backs the loan; the lender issues it. Key details:

- No down payment required for eligible borrowers.

- Must be a U.S. citizen, U.S. non-citizen national, or qualified alien, and must occupy the home as a primary residence.

- 30-year fixed rate only; no adjustable-rate option.

- Household income cannot exceed 115% of the area median income.

- USDA does not set a minimum credit score, but most participating lenders require a score of 640.

- No waitlist. Applications are accepted on a rolling basis.

For most buyers building with Value Built Homes, the Guaranteed Loan is the practical option. It’s widely available through approved lenders, and it doesn’t require waiting.

USDA Single Family Housing Direct Loan Program

The Direct Loan is issued by USDA directly, not through a private lender. It serves lower- and very-low-income households and carries a lower base interest rate. As of April 1, 2026, the rate is 5.00% for qualifying borrowers, with payment assistance options that can reduce the effective rate to as low as 1%.

The Direct Loan was built for buyers in rural areas for whom affordable homeownership would otherwise not be possible. That mission is reflected in the program’s own description, which frames it as a path to ownership specifically for families who have no other realistic way to get there. The Guaranteed Loan, by contrast, extends eligibility to moderate-income households as well, which is why it’s the more accessible starting point for most Value Built Homes buyers.

One practical consideration: processing times for the Direct Loan vary by location and funding availability, and USDA does not publish a fixed wait time. For current timelines in Southwest Indiana, contact the Jasper Area Office at 812-482-1171, Ext. 4 before planning around the Direct program. If timing is a concern, the Guaranteed Loan processes through private lenders and has no waitlist.

Can You Use a USDA Loan for New Home Construction?

Yes. USDA financing can be used for new construction through a Single-Close Construction-to-Permanent loan. This structure combines the construction loan and the permanent mortgage into one closing, which simplifies the process and can reduce the total closing costs compared to two separate loans.

A few requirements apply specifically to new construction:

- Owner-builders are not permitted. The home must be built by a third-party contractor vetted and approved by the participating lender.

- USDA does not maintain an approved builder registry. The lender approves the builder through license verification, insurance validation, a credit review, reference checks, and a criminal background check.

- A fixed-price construction contract is required. Contingency reserves up to 10% of construction costs are permitted.

- Construction ends with a final inspection and a certificate of occupancy before the loan converts to a 30-year fixed mortgage.

One important constraint: the single-close construction loan is currently offered by only 21 lenders nationally. USDA maintains an updated list of participating lenders. Confirming that a lender serving Indiana is on that list should be one of your first steps before pursuing this path.

Value Built Homes serves as the contractor in this scenario. Buyers arrange their own financing through a USDA-approved lender. Value Built Homes does not provide USDA loans. For a broader look at how construction loan documentation and lender requirements work in Indiana, Indiana Construction Loan Requirements: Avoid Delays covers the preparation steps in detail.

How Value Built Homes’ Price Points Work with USDA

The USDA Guaranteed Loan program does not set a hard maximum loan amount, but the purchase price must be reasonable relative to the appraised value. In practice, home prices in the range that Value Built Homes builds fall well within what USDA-eligible buyers in Southwest Indiana typically finance.

Value Built Homes builds affordable site-built homes across six active subdivisions in Gibson, Posey, Warrick, Knox, and Vanderburgh counties. Current floor plan pricing ranges from $128,500 to $238,000 depending on the plan. (Verify current pricing on the floor plans page before referencing specific figures, as pricing may change.)

Value Built Homes also offers a Free Construction Financing program that covers the interest on the construction loan during the build phase. This program comes from Value Built Homes, not from USDA. The two financing components serve different purposes: USDA covers the permanent mortgage; Value Built Homes’ program covers construction-phase interest costs. For a detailed look at how construction financing works in Southern Indiana, including how draws and timelines affect the process, Construction Loan Questions Every Southern Indiana Homebuyer Should Ask is a useful companion read.

Does Your Location Qualify? How to Check USDA Area Eligibility

Rural area eligibility is determined at the property address level, not by county or zip code. A lot in one part of a county may qualify while another does not. This means you need to verify your specific address before making assumptions.

Value Built Homes builds in Princeton, Poseyville, Boonville, and Vincennes, smaller communities that are likely to qualify based on their population and rural character. Evansville is a larger city, and eligibility for specific addresses within the metro area varies. Use the USDA Property Eligibility Map to check any specific address or lot before you get too far into planning.

Income eligibility is a second requirement. For Guaranteed Loan borrowers, household income must fall at or below 115% of the area median income for your county. For all five counties in Value Built Homes’ active service area (Gibson, Posey, Warrick, Knox, and Vanderburgh), the current USDA Guaranteed Loan income limits are $119,850 for households of 1–4 people and $158,250 for households of 5 or more as of FY2025. Use the tool to confirm current figures for your county before applying, as limits update annually.

Local USDA Contact for Southwest Indiana

If you want to explore eligibility or discuss the Direct Loan program directly with USDA, the Jasper Area Office serves Gibson, Posey, Warrick, Knox, and Vanderburgh counties:

- Address: 1484 Executive Blvd, Jasper, IN 47546-9300

- Phone: 812-482-1171, Ext. 4

The Jasper office can confirm area eligibility, explain current income limits, and walk through program requirements for your specific situation.

Frequently Asked Questions About USDA Loans for New Home Construction in Indiana

Can you build a new home with a USDA loan?

Yes. USDA financing can be used for new construction through a Single-Close Construction-to-Permanent loan. Owner-builders are not permitted; the home must use a third-party contractor approved by the participating lender. The lender vets the builder through license verification, insurance validation, a credit review, and a background check. Construction requires a fixed-price contract and ends with a final inspection and certificate of occupancy before the loan converts to a 30-year fixed mortgage.

What is the difference between the USDA Guaranteed and Direct loan programs?

The Guaranteed Loan is issued through private lenders and serves moderate-income buyers with household income up to 115% of the area median. It has no waitlist. The Direct Loan is issued by USDA directly and serves lower-income households with a lower interest rate and payment assistance options. Processing times for the Direct Loan vary by location and funding availability; contact the Jasper Area Office at 812-482-1171, Ext. 4 for current timelines in Southwest Indiana.

Does USDA allow new construction in Indiana?

Yes. USDA financing is available for new construction in Indiana through the single-close construction loan option. Property eligibility is verified at the address level. Use the USDA Property Eligibility Map to confirm whether your specific address qualifies before planning around it.

How many lenders offer the USDA construction-to-permanent loan?

Only about 21 lenders nationally participate in USDA’s single-close construction loan program as of the most recent lender list. Identifying an Indiana-based lender that offers this specific product is one of the first practical steps in the process.

Does Value Built Homes work with USDA-financed buyers?

Value Built Homes is the builder, not the lender. Buyers arrange their own financing, including USDA loans through an approved lender. Value Built Homes does not offer USDA loans directly. If you’re exploring USDA financing for a Value Built Homes project, contact the team to discuss how the builder-lender relationship works in practice.

Ready to Explore Your Options?

For buyers in Southwest Indiana looking at zero-down financing for new construction, USDA loans are a financing option worth understanding. Value Built Homes’ floor plans and service area align well with what USDA-eligible buyers in this region typically finance.

Browse Value Built Homes’ floor plans to find a home that fits your budget, or contact the Value Built Homes team to talk through your situation and next steps.