Securing a construction loan in Indiana may seem complex, but with the right preparation and a clear understanding of lender requirements, you can confidently meet expectations and start building your dream home. This guide explains each requirement in simple language and offers a practical, step-by-step checklist to ensure your application is complete and compelling. Whether you’re a first-time homebuyer or looking to build on your land, this roadmap is designed to help make the process both efficient and manageable.

In the sections below, you’ll discover detailed lender expectations, explanations of important financial concepts, and clear directions on preparing all necessary documentation. Let’s begin by understanding some of the challenges that can delay construction loan applications in Indiana and what you can do to avoid them.

Construction Loan Types in Indiana (Construction-Only vs. Construction-to-Permanent)

Before you apply, know which loan structure you’re using. In Indiana, most borrowers choose either construction-only or construction-to-permanent (often in a one-time close/single-close format).

Construction-Only: Two-Step Financing

A construction-only loan covers the build phase (commonly 6–18 months) and is funded through a draw schedule. Payments are usually interest-only on the amount drawn. After the home is complete, you must apply for a separate mortgage to pay off the construction loan.

- Pros: flexibility to shop mortgage rates later

- Cons: typically two closings, possible rate changes, and you may need to qualify twice

Construction-to-Permanent

A construction-to-permanent loan starts as a construction loan (draws during the build) and then converts into a long-term mortgage when the home is finished.

- One-time close (single-close): close once upfront; converts without a second closing

- Two-close: close on the construction loan first, then a second closing for the mortgage

Ask lenders: Is it one-time close or two-close? Will I re-qualify at conversion? Can I lock my rate upfront (and for how long)?

Why Construction Loan Applications Face Delays in Indiana

Delays often occur because of various local challenges that impact your loan application:

- Local Permitting and Zoning Issues: Each county or city has its own rules regarding building permits. Failing to secure these permits early can delay your approval.

- Incomplete Documentation: Lenders expect comprehensive details such as architectural plans, an itemized budget, and signed builder contracts. Incomplete or inconsistent documentation forces lenders to request additional information, which can push back the process.

By understanding these challenges and preparing all necessary documents early on, you can help maintain momentum in your loan process.

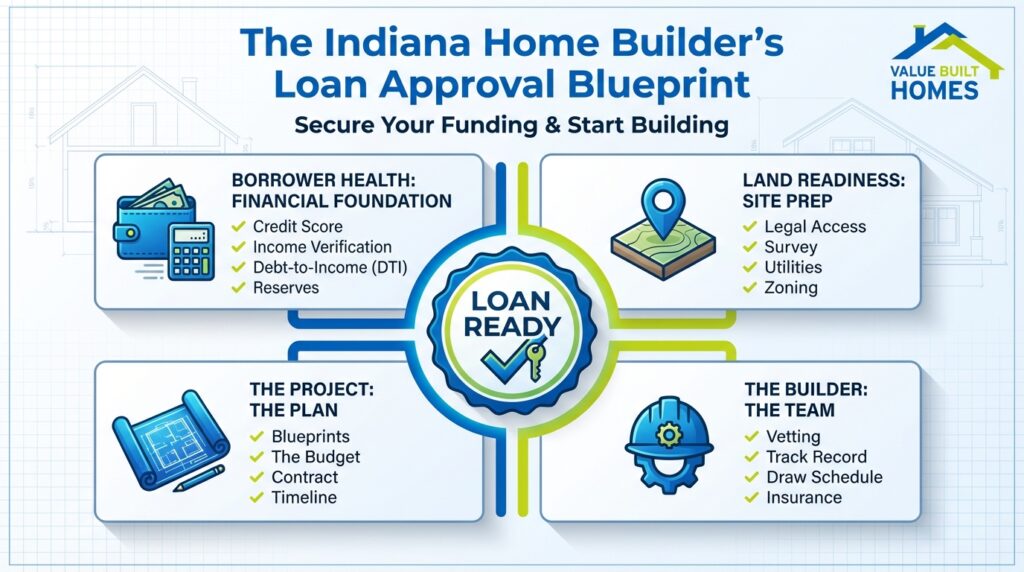

Understanding Lender Expectations: A Multi-Factor Approach

Lenders review several key components to assess the overall risk of your project. These components need to align to build a strong case for approval:

- Borrower: Lenders assess your financial health by examining your credit score, employment history, debt-to-income ratio (DTI)—the percentage of your monthly income that goes toward paying debts—and cash reserves. A healthy credit score, typically in the mid-600s or higher, is important for demonstrating your trustworthiness, and higher scores can offer better financial opportunities.

- Land: Your property must be suitable for building. Lenders will verify that there is proper legal access, review surveys (ensure you have an updated survey), clear easements, and ready utility setups. Compliance with local zoning and building codes is essential.

- Builder: A reputable, licensed builder is crucial. Lenders require details that verify you have engaged a reputable, licensed builder with a proven track record.

- Project Plan and Budget: Detailed, professional architectural and engineering plans, along with a realistic budget that includes a “cost-to-complete” estimate, are required. Additionally, a draw schedule—a timeline that aligns loan disbursements with specific construction milestones—helps ensure that funds are used appropriately.

Each pillar must be strong to minimize risk and contribute to a smooth approval process.

Borrower Requirements: Demonstrating Your Financial Strength

Lenders look closely at your financial stability. Here is what you need to prepare:

Credit Score and Financial Health

A healthy credit score, typically in the mid-600s or higher, is important for demonstrating your trustworthiness as a borrower. To improve your score, settle outstanding debts and review your report for accuracy.

Income and Employment Stability

Lenders need proof of steady income. For traditional employees, W-2 forms and recent pay stubs are usually sufficient. For self-employed individuals, be prepared to provide two years of tax returns and profit-and-loss statements. A consistent employment history increases lender confidence.

Simplifying Financial Metrics

- Debt-to-Income Ratio (DTI): This figure shows how much of your monthly income is committed to existing debt. Lenders prefer lower ratios because they indicate you have more disposable income available to handle new loan payments.

- Cash Reserves: These funds in savings or other liquid assets show that you can manage unexpected expenses during construction. Robust reserves are especially important during the interest-only phases of construction loans.

Down Payment and Land Equity

For many conventional loans, down payments typically range from about 5% to 20%. However, some loan programs offer options with as little as 3% down, and specialized loans such as VA or USDA programs may allow for zero down. If you already own the land, its equity can help reduce your cash requirements. Be sure to have recent appraisals or other documentation confirming your land’s value.

Project Requirements: Crafting a Solid Build Plan

Once your financial foundation is secure, the next step is to prepare a robust project plan.

Comprehensive Plans and Budget

Your architectural and engineering plans must be clear, detailed, and in compliance with local building codes. A realistic, itemized budget should include:

- Hard Costs: Materials and labor.

- Soft Costs: Permits, design fees, and engineering expenses.

The Construction Contract

A well-drafted construction contract is essential. This document should clearly outline:

- The scope of work.

- The project timeline.

- Detailed cost estimates.

Common contract types include:

- Fixed-Price Contract: Offers a set cost to reduce uncertainty.

- Cost-Plus Contract: Provides flexibility, although it may require closer oversight of additional expenses.

Draw Schedule and Milestones

A draw schedule segments the project into defined milestones (for example, foundation, framing, roofing) and aligns them with the disbursement of funds. This structure not only secures the lender’s interest but also helps you manage the project budget effectively.

With a strong project plan in place, the next critical step is ensuring that your property meets all necessary build requirements.

Land and Property Requirements in Indiana

Your property must prove that it is ready for construction. Here’s what you need to focus on:

Ensuring Buildability

Confirm your property has legal access to roads and meets zoning requirements:

- Obtain an updated survey that clearly shows boundaries, easements, and access routes.

- Pre-established easements can help prevent delays later in the process.

Addressing Infrastructure Considerations

For properties in rural areas or locations with limited infrastructure, it’s important to verify all available documentation related to utility setups or alternative service arrangements. In some cases where municipal utilities are not available, you may need to secure permits and documentation for alternatives such as private wells.

Navigating Local Permits

Every locality has its own processes for permitting. Work closely with your builder to ensure that you:

- Secure all necessary building, zoning, and environmental permits well in advance.

- Understand local rules and regulations to avoid any last-minute surprises.

Documentation Checklist: Getting “Loan-Ready”

To ensure a smooth application process, prepare and organize the following essential documents:

Personal Financial Documents

- Current pay stubs or profit-and-loss statements.

- Tax returns for the past two years.

- W-2 forms (if applicable) for the last two years.

- Bank statements showing available cash reserves.

- Documentation for any additional income sources (e.g., rental income).

Employment and Income Verification

- A letter verifying current employment (VOE).

- For self-employed individuals: Business tax returns and profit-and-loss statements.

Land and Property Documents

- Deed or purchase agreement for the land.

- An updated survey showing boundaries and easements.

- Documentation for any relevant property tests or permits, if applicable.

Builder Documentation

- A signed construction contract that details the project scope, timeline, and cost estimates.

- A draw schedule linking key construction milestones to funding disbursements.

- Proof of the builder’s licensing, experience, and insurance coverage.

Insurance and Permits

- Builder’s risk insurance policy.

- General liability insurance (if required).

- Copies of all approved permits and zoning confirmations.

With all documentation assembled, understanding how payments work during construction can help maintain your project’s budget and timeline.

Payment Requirements During Construction

Understanding the payment structure can help you avoid budgetary surprises:

Interest-Only Payments

Most construction loans are set up as interest-only during the build phase. This arrangement means that you initially pay only the interest-only payments on the funds you draw, making early payments more manageable. As construction progresses, the payments will increase as more funds are disbursed. To ease this burden, Value Built Homes offers a free construction financing program that covers interest payments during construction—potentially saving you thousands of dollars.

Managing Overlapping Housing Expenses

Many borrowers need to maintain their current residence while building a new home. Lenders take these overlapping expenses into account, so it’s important to budget carefully to cover both sets of costs.

Streamlining Financial Management

Working with builders who offer standardized, transparent pricing and home designs can minimize unexpected cost overruns. This predictability in budgeting supports a smoother overall financial process throughout the project.

Pre-Approval Timeline for Indiana Builds

Maintaining a clear, organized timeline is essential. Follow this week-by-week checklist to keep your application process on track:

- Weeks 1-2: Gather all financial documents, review your credit report, and finalize land details.

- Weeks 3-4: Collaborate with your builder to secure preliminary plans and permits; submit these documents for an initial lender review.

- Weeks 5-6: Arrange for a property appraisal and finalize your detailed project budget, including builder documentation.

- Week 7: Respond promptly to any lender requests and aim to obtain your pre-approval decision.

Remaining organized and proactive during these weeks will help you avoid common pitfalls and ensure a smooth pre-approval process.

Tools to Simplify the Loan Process

Effective organization is key. Consider these two tools to streamline your preparation:

Document Checklist

Keep a detailed checklist of all required documents. This simple tool prevents any last-minute scrambles and demonstrates your commitment to presenting a complete, professional application to the lender.

Loan Readiness Scorecard

Evaluate your application’s overall strength by reviewing these critical areas:

- Borrower Readiness: Confirm your credit score, manageable DTI, and stable income.

- Land Readiness: Verify legal access, obtain up-to-date surveys, and ensure zoning compliance.

- Builder Readiness: Ensure that you have a signed contract and a clear, milestone-based draw schedule.

- Project Budgeting: Review your cost estimates and include contingencies for unexpected expenses.

Using these tools, you can identify and address any weak points before submitting your application, which helps increase lender confidence.

Final Loan Approval and Closing

Once pre-approval is secured, your loan moves toward final approval and closing. During this final phase:

- Review of Terms: Carefully examine the interest rate, draw schedule, and repayment terms to ensure they align with your budget.

- Initial Draw Request: Submit the necessary documentation for the first disbursement, typically covering foundational work.

- Inspection and Verification: Collaborate with your builder and the lender to confirm that each construction milestone has been completed satisfactorily before funds are released.

Clear communication during this phase is essential for a smooth transition from loan approval to construction and, ultimately, to moving into your completed home.

FAQ: Indiana Construction Loan Requirements

What credit score do I need for a construction loan in Indiana?

Many lenders look for a mid-to-high 600s credit score or higher, with stronger terms often available to borrowers with higher scores. Exact minimums vary by lender and loan type.

How much down payment is required for an Indiana construction loan?

Down payment requirements vary, but many programs fall in the 10%–20% range. If you already own your land, land equity may count toward your down payment, depending on the lender’s rules and appraisal.

Can I use land as a down payment (land equity) in Indiana?

Often, yes. If you own the lot free and clear (or have significant equity), lenders may allow that equity to be applied toward your required cash investment—usually based on an appraisal and title review.

What documents do I need to apply for a construction loan?

Common requirements include income/asset documentation (pay stubs, tax returns, bank statements), plus build-specific items like construction plans, an itemized budget, a signed builder contract, and a draw schedule.

What is a draw schedule, and how do draws work?

A draw schedule breaks construction into stages (foundation, framing, etc.). The lender releases funds (“draws”) after milestones are completed—often with an inspection or verification before each disbursement.

What’s the difference between construction-only and construction-to-permanent (one-time close) loans?

- Construction-only: finances the build, then you apply for a separate mortgage later (usually two closings).

- Construction-to-permanent: converts from construction financing into a mortgage when the home is complete. A one-time close/single-close version closes once upfront and converts without a second closing.

Efficiently Navigating Indiana Construction Loan Processes

Meeting Indiana’s construction loan requirements means preparing a thorough application that covers every detail—from your personal financial status and solid project plans to having every necessary document in order. With a well-organized approach, clear explanations of key financial concepts, and a carefully planned timeline, you can set the stage for an efficient, stress-free home-building journey.

Embrace proactive planning and utilize practical tools such as document checklists and a loan readiness scorecard to strengthen your application. Now is the time to take action—build confidence, eliminate delays, and start constructing the home you’ve always envisioned.

Ready to experience a streamlined and stress-free home-building process? Contact Value Built Homes today to take the first step toward turning your Indiana dream home into reality.