Building your dream home in Indiana is an exciting journey, but financing it can feel overwhelming. Unlike buying an existing house, you can’t use a traditional mortgage. Instead, you’ll need a construction loan—special financing designed to cover everything from labor and materials to permits, releasing funds as your build progresses.

The most important decision you’ll make is choosing the right type of construction loan. Most homebuyers in Indiana will choose between two primary options: the one-time close construction loan and the two-time close construction loan. While they serve the same purpose, their differences in structure, cost, and flexibility can significantly impact your budget and stress levels.

At Value Built Homes, we specialize in helping Indiana homebuyers navigate this process with simplified floor plans and efficient construction. This guide will break down the features, benefits, and drawbacks of each loan, helping you decide which option is the perfect fit for your dream home.

What Is a One-Time Close Construction Loan?

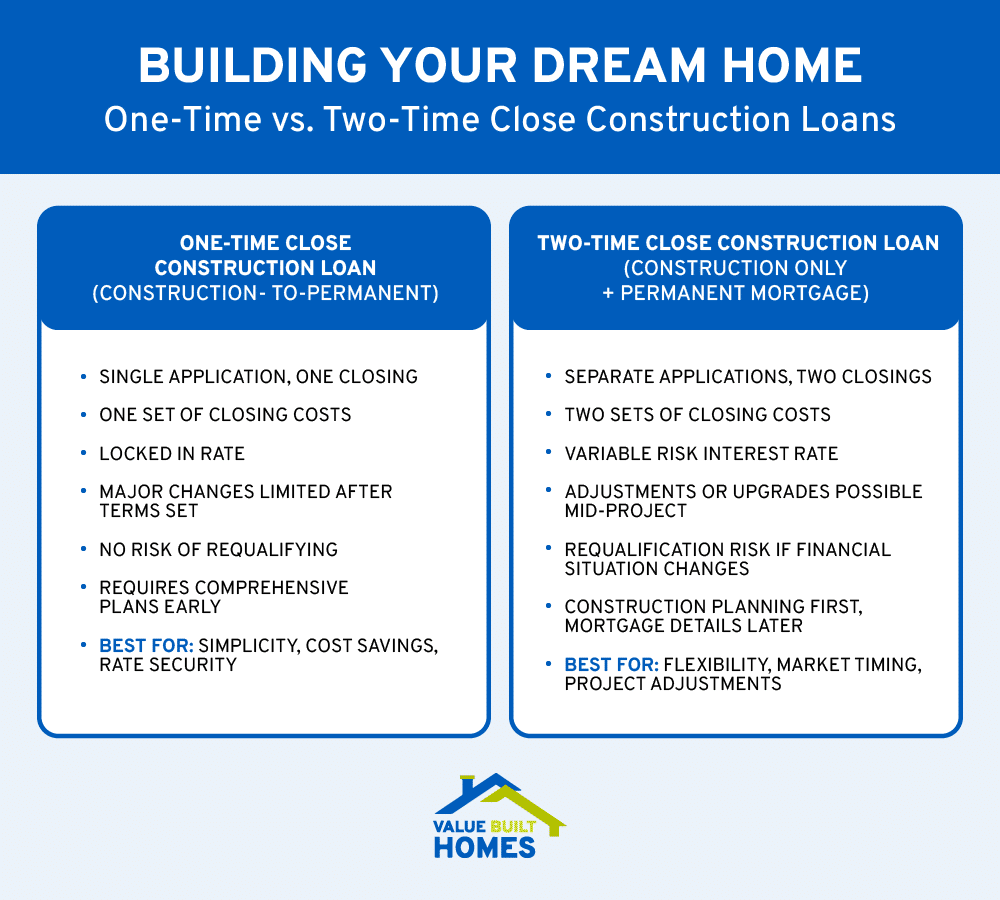

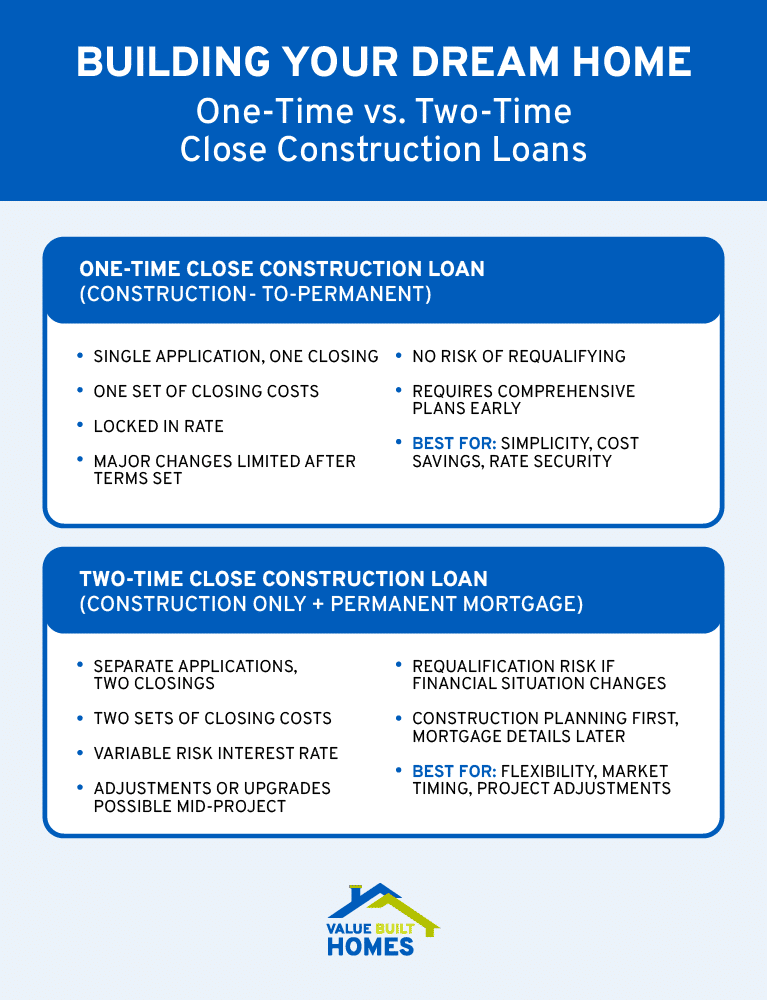

A one-time close construction loan—also known as a construction-to-permanent loan—combines the entire financing process into one seamless transaction. From application to closing, you only deal with one underwriting process, one set of fees, and one closing. Initially, the loan finances the construction of your home. Once construction is complete, the loan converts into a permanent mortgage, typically featuring fixed terms and a fixed interest rate.

Key Features

- Single Application and Closing: Only one set of paperwork, fees, and closing procedures is required.

- Unified Financing: Construction costs and long-term mortgage are combined into one loan.

- Fixed Interest Rate: Your rate is locked at the outset, offering protection against market fluctuations.

- Upfront Planning: A detailed construction plan and cost estimate are required during the application process.

- Streamlined Process: Fewer administrative tasks reduce stress for first-time homebuilders.

If you’re looking for more general insights into construction loan structures, check the Consumer Financial Protection Bureau guidelines.

How It Works

- Application and Approval: You provide financial documents, construction plans, and property details. Lenders review your credit, income, and project specifics.

- Single Closing: Upon approval, you sign all necessary documents at one closing, and fees are paid.

- Construction Phase: Funds are released in draws as specific construction milestones are met. Inspections ensure that progress aligns with the plan.

- Conversion: Once construction is complete, the loan automatically transitions to a permanent mortgage with predefined terms.

Benefits and Challenges

Benefits:

- The simplified process reduces paperwork and administrative costs.

- Locking in an interest rate at the start protects against future rate increases.

- Eliminates the risk of having to requalify for a separate mortgage after construction.

Challenges:

- Requires a comprehensive construction plan and cost estimates upfront, which can increase initial costs.

- Less flexibility for making major changes to the project once the loan terms are set.

- Stricter qualification standards might apply, as lenders evaluate both construction and permanent financing together.

What Is a Two-Time Close Construction Loan?

In contrast, a two-time close construction loan separates financing into two distinct stages. Initially, you receive a short-term construction loan to cover the build. After the home is finished, that loan is paid off when you secure a separate permanent mortgage. This option can offer flexibility but generally comes with additional fees and administrative tasks.

Key Features

- Separate Loans: One loan funds the construction phase, and another provides long-term financing.

- Two Closings: Each phase requires its own application, underwriting, and closing processes.

- Flexible Terms: The first loan is short-term and may include adjustable rates, while the permanent mortgage is chosen later.

- Potential for Better Rates: Securing the permanent mortgage after construction allows you to obtain terms that might reflect updated market conditions.

How It Works

- Construction Loan Application: You apply for a short-term loan with documentation similar to the One-Time Close option.

- First Closing: The construction loan is finalized, with funds disbursed in draws as milestones are met.

- Construction Phase: Interest-only payments are often made on the construction portion until completion.

- Permanent Mortgage Application: Once the project is done, you apply for a separate long-term mortgage.

- Second Closing: After approval, the chosen mortgage pays off the construction loan.

Advantages and Disadvantages

Advantages:

- Greater flexibility during construction allows adjustments or upgrades as needed.

- Opportunity to secure potentially better permanent mortgage terms based on evolving market conditions.

- May be easier to qualify for an initial short-term loan, then requalify for a permanent mortgage later.

Disadvantages:

- Higher overall costs due to two closing processes and fees.

- Risk of not qualifying for the permanent mortgage if your financial situation changes.

- Potential for increased interest rates if the market rises during or after construction.

Who Is the Ideal Candidate for Each Loan?

Choosing the right loan often comes down to your personality, financial situation, and how you approach planning. See which of these profiles sounds most like you.

You’re a great candidate for a one-time close loan if…

- You value certainty and simplicity. You have a detailed plan for your new home and don’t expect to make major changes. Your priority is a streamlined, predictable process with fewer administrative hurdles.

- You want to lock in your costs now. You are budget-conscious and want to avoid the expense of a second closing. Locking in your interest rate from the start gives you peace of mind against market volatility.

- You are a first-time homebuilder. The single-closing process is often less intimidating and easier to manage if you’re new to the world of construction financing.

- Your financial picture is clear and strong. You have a stable income and a good credit score, allowing you to qualify for both the construction and permanent financing phases at the same time.

You might be better suited for a two-time close loan if…

- You want maximum flexibility. You anticipate making adjustments or significant upgrades during the construction process and need a loan structure that can accommodate those changes.

- You are willing to bet on the market. You believe interest rates might decrease by the time your home is built, and you want the freedom to shop for the best possible rate on your permanent mortgage. You can monitor market conditions using resources like the Freddie Mac’s updated mortgage rate data.

- Your financial situation might improve. Perhaps you’re expecting a salary increase or your credit score is on the rise. Separating the loans allows you to re-qualify for the permanent mortgage later, potentially securing better terms.

- You are an experienced builder or have a complex project. You are comfortable navigating two separate application and closing processes to gain more control over the financing terms.

How Value Built Homes Simplifies the Process

At Value Built Homes, we understand these factors deeply. As dedicated Indiana home builders, we design our entire process to align with the efficiency and peace of mind that a one-time close loan offers. By providing simplified floor plans to reduce decision fatigue and a quick construction process for our high-quality site built homes, we help you navigate the financing journey with confidence and ease.

Frequently Asked Questions (FAQ)

What is a typical credit score needed for a construction loan?

Most lenders look for a credit score of 680 or higher for a construction loan, with some preferring a score of 700 or more. Because the lender is financing a home that doesn’t exist yet, the qualification standards are typically stricter than for a standard mortgage.

How much of a down payment is required?

A down payment of 20-25% is standard for most conventional construction loans. However, government-backed programs can offer lower down payment options. For example, FHA construction loans may require as little as 3.5% down, and VA construction loans may require 0% down for eligible veterans.

Can I use the construction loan to buy the land?

Yes, you can often roll the cost of purchasing the land into your total construction loan. This is a common feature of one-time close loans, which finance the lot, construction, and mortgage all in one package. If you already own the land, you can often use the equity you have in it as part of your down payment.

What happens if my project goes over budget?

Cost overruns are typically the borrower’s responsibility to pay out-of-pocket. Your loan is approved for a specific amount, and the lender will not automatically increase it. This is why it is crucial to build a contingency fund—usually 10-15% of the total construction cost—into your initial budget to cover any unexpected expenses.

Are there special programs for Indiana homebuyers?

While Indiana does not have its own specific construction loan programs, Indiana homebuyers can take full advantage of federal options like FHA, VA, and USDA construction loans. Working with a builder and lender who are experienced in the Indiana market is the best way to navigate your options and find a loan that fits your project.

Deciding on Your Path to Homeownership: Simplified Versus Flexible Construction Loan Options

Choosing the right construction loan is a critical step in turning your dream home into a reality. The one-time close construction loan simplifies the journey by combining construction and permanent financing into one seamless process, offering cost savings, interest rate security, and administrative efficiency. Conversely, the two-time close construction loan provides more flexibility—particularly useful when you anticipate significant changes during the build—but it can increase overall fees and complexity.

Ultimately, your decision will hinge on your financial readiness, the complexity of your project, and your preference for simplicity versus flexibility. Contact Value Built Homes today to learn how our stress-free approach to new home construction and financing can help you achieve your dream home.